It’s my favorite goals of the year, financial goals! Since college, I’ve been obsessed with tracking my finances, debt, and plans. And now with a steady income and organized bills and all, I’m finally ready to take action and start taking on my finances this year and actually making progress towards my goals.

I always stay as open as I can on the blog, and I think it’s so important to be open when it comes to money.

Short Term Goals

Fill my emergency fund

I was always so proud of my emergency fund. It was well stocked, in a HYSA, and I didn’t touch it for months. In the past two years though, I have spent some time living off of my emergency fund, leaving it empty. I’d like to have a minimum of 3 months of my recurring expenses in my emergency fund by the end of the year. Realistically, I’ll need more than just the recurring expenses, but this makes the goal more attainable and covers the things I absolutely need.

Three months of recurring expenses mean $4,500 in my emergency fund. Right now I have about $1,400 already saved, which comes to around $250 per month needed to get to my goal amount. I think it’s a little more of a stretch goal for my budget, but let’s see how I do!

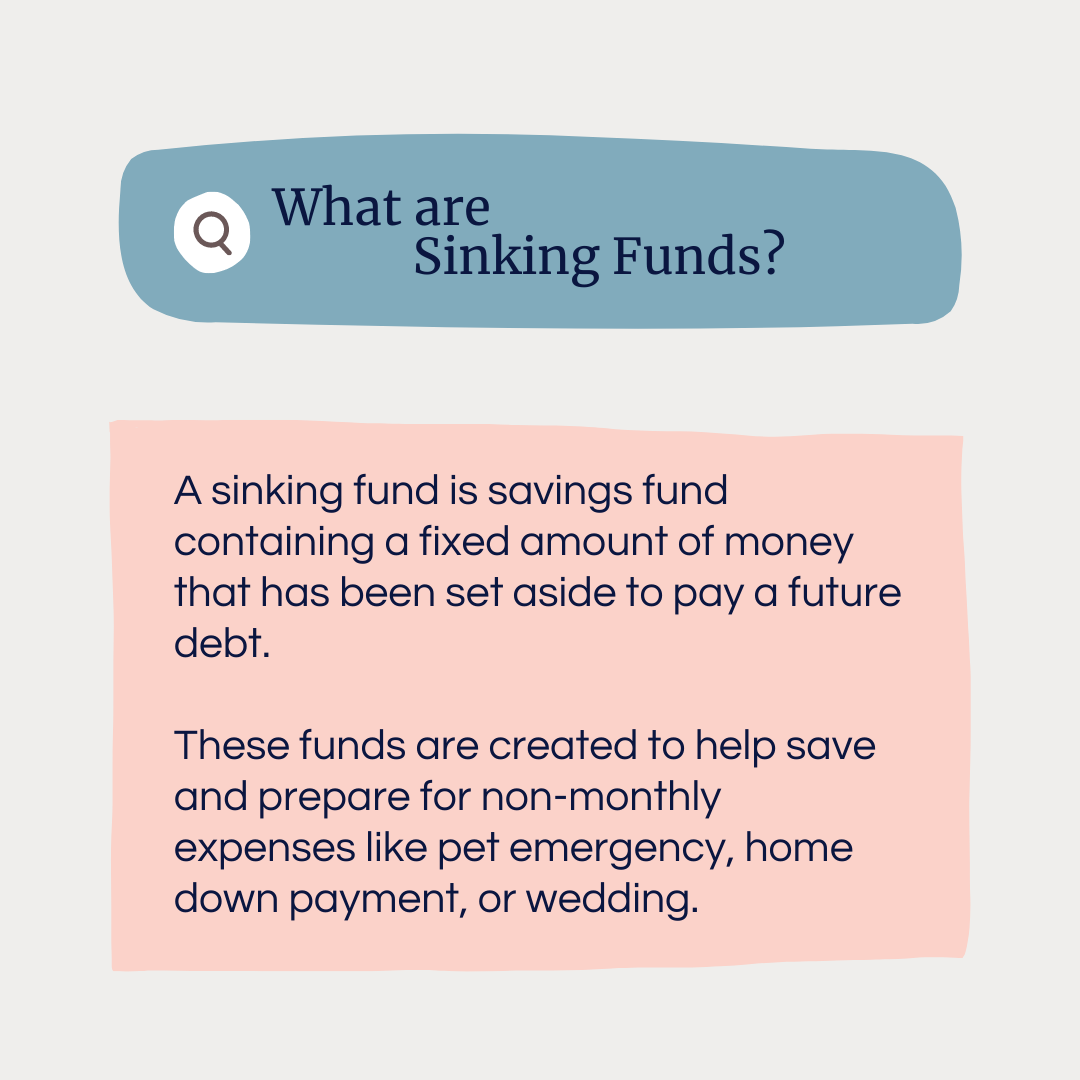

Fill my Sinking Funds

A big goal is to refill my sinking funds. When I emptied my emergency fund, I ultimately pulled from my other funds to make everything work. Now that I’m rehabbing my savings, it’s time to put some money back into it all. I have 3 sinking funds; Levi, Car, and Apartment.

Levi’s sinking fund is set aside for emergency vet visits. This fund is technically full at $600, and Cody has his own sinking fund for Levi too. I’d like to bump this fund up a little to 1,000, just in case!

The Car fund is a pretty self-explanatory one, just designed to save up for any major expenses for my car that aren’t covered under the warranty. Right now this fund has a whopping $50 in it. I’m not sure what my ultimate goal amount is, but I’m going to start with $500, to cover the highest car insurance deductible.

The Apartment fund is to cover a down payment for an apartment if I have to start going into the office. I’ve been really lucky to have a job that allows me to work remotely. That might not be the case forever, so I’d like to have a little put away for this. The average cost of a 1 bedroom apartment is a little over two thousand a month, which means the down payment would be around four to five thousand. Luckily, I’d be splitting this with Cody, so I think I’m going to work up to $3,000 in this sinking fund. That would cover one month with a little leftover to go towards other moving expenses.

Pay off one Stafford loan

I carry a lot of student debt. Not the most debt in the world, but it’s a lot to me and it’s pretty impactful on me. I have $55,487.35 in student loans, across two types of loans. About half was in a private loan from a New Jersey program that I refinanced with Earnest, and the other is in federal Stafford Loans. I’d love to just send in one whole year of salary and be done with all this debt, but unfortunately that’s not how it works. So it’s my goal to pay off one Stafford Loan this year. They are the smaller loans, but they also have the highest interest rates. I’m focusing on a 5.05% interest rate loan that has a $5,500 balance. That being said, I’m still holding onto the payments until we actually have to pay them again, so more than happy to have those payments on hold for now!

Improve my Net Worth

My current net worth sits around -$69,944 which is a pretty scary number, thanks to two hefty debt categories, my student debt ($55,500) and my car loan ($21,000). I have a plan to pay down that debt, which will improve my net worth, but I want to continue to invest in myself and continue to grow my net worth in more positive ways.

I invest 3% of my paycheck into a 401K through my job, but I also have a Wealthfront Investment Account. Last year I tried to invest in it regularly, but only ended up making one deposit and fell off the bandwagon. This year, I reorganized my budget and getting back to it. I carved out $130 a month in my budget, matching my 401K investment.

If everything goes exactly to plan, between debt payment and investments, I’ll be increasing my net worth by over $16,000 this year. At least that’s the goal.

Long Term Goals

In terms of long term financial goals, I really don’t have many. Obviously things like paying off my loans, save enough for retirement, and eventually we want to buy a home. Otherwise I’m more than content to focus on my shorter term goals for the time being.

Sound off in the comments with your financial goals for 2022!